Mismanaging Your Cashflows as a BigLaw Partner Could Be Costing You Millions!

Written by Chris DeVito

Most partners assume they’re doing the right thing by maxing out their 401(k), profit-sharing, & Cash Balance Plan contributions, and then dropping their year-end distribution into the market in one big chunk. It feels organized. Clean. Efficient.

But what if the very way you’re structuring those inflows is quietly costing you millions over your career?

The Real Cost of Poor Cashflow Management

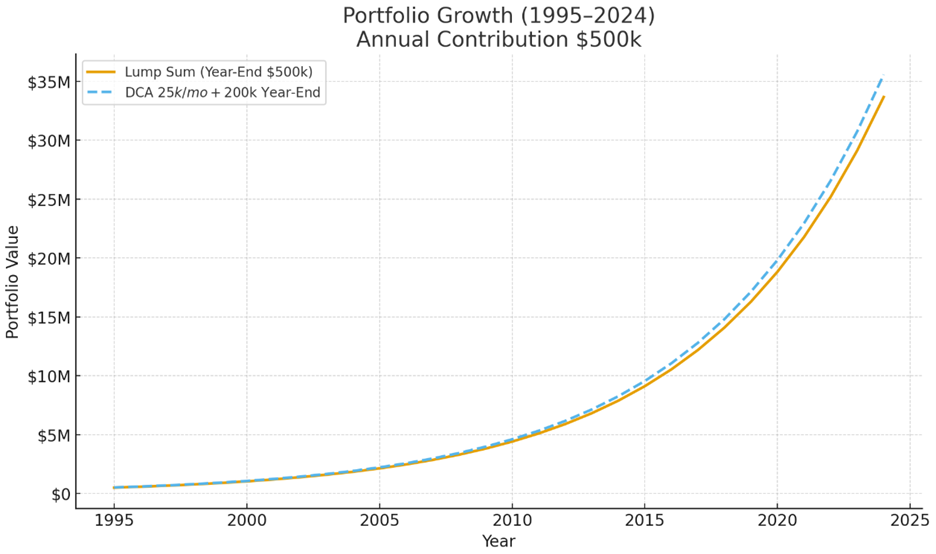

We recently ran a 30-year analysis using real S&P 500 total return data (1995–2024) to test two common investment behaviors:

- Year-End Lump Sum: Contributing $500,000 on the last trading day of each year (mirroring how many partners think about deploying bonus or distribution dollars).

- Structured Cashflow Strategy: Contributing $25,000 per month (on the first trading day) plus $200,000 at year-end — a setup that mirrors a disciplined “cashflow-aware” approach.

Both methods invested the same $500,000 annually. The only difference was when the dollars hit the market.

The Results: $1.9 Million Left on the Table!!!

After 30 years:

- Lump Sum Strategy Final Value = $33.7M

- Cashflow-Aware Strategy Final Value = $35.6M

- Difference = +$1.9M in favor of “Cashflow Aware”.

Disclosure: This hypothetical example is used for illustrative purposes only and is not representative of actual resus.

Why Timing Matters So Much

- Earlier Market Exposure: Dollars invested monthly start compounding right away instead of sitting in cash until December.

- Dividend Reinvestment Advantage: Reinvested dividends on those early contributions snowball over time.

- Behavioral Discipline: Spreading allocations smooths volatility and enforces a systematic discipline Partners often lack when life and practice get in the way.

What This Could Mean For You

If you’re like most high-income attorneys, you have:

- Big quarterly draws,

- Significant annual distributions, and

- Multiple competing cash demands (taxes, lifestyle, buy-ins, and capital calls).

Without a personal CFO structure around when and how those flows are deployed, you risk leaving seven figures on the table over your career.

This isn’t about chasing the next hot investment. It’s about being ruthlessly efficient with what you already earn.

The Final Verdict?

The difference between “organized but sub-optimal” and “strategically managed” cashflows isn’t measured in basis points. It’s measured in actual dollars.

As an AM 100 Partner, you’ve already done the hard part — earning. The next level is ensuring those dollars are deployed in the most tax-aware, compounding-efficient way possible.

Question to ask yourself: Do you have a framework ensuring every dollar you earn is working for you as soon as possible? Or is your current system quietly leaking millions over time?

Disclosure: The opinions expressed, and materials provided are for general information and should not be considered a solicitation for the purchase or sale of any security. Past performance is not a reliable indicator of future results.

All investing involves risk including the possible loss of principal. No strategy assures success or prevents loss.

Dollar-cost averaging cannot assure a profit or protect against loss in a down market.

8393412RG_Sep27