How Big Law Partners Are Leaving Hundreds of Thousands on the Table

The Hidden Cost of Playing It Safe

If you're a partner at a Big Law firm, you've likely mastered the art of complexity, navigating high-stakes deals, managing client relationships, and attention to detail that is second to none. But when it comes to your own finances, one understandable habit may be quietly costing you hundreds of thousands of dollars.

The Problem: Uncertainty Breeds Excess Cash

Here's a scenario most Big Law partners know well: your income isn't fully predictable. Quarterly tax estimates are due before you even know what your draw will look like. Your CPA gives you a rough number, but there's a wide margin of error. So, what do you do?

You keep cash. A lot of it.

It feels responsible. It feels smart. And honestly, in the short term, it is, you need liquidity for tax payments, capital calls, and unexpected expenses. But the problem isn't keeping some cash. The problem is keeping far more than you actually need, for far longer than necessary.

Many partners we speak with are holding close to $500,000 or even $1,000,000 in cash or near-cash instruments at any given time, when their actual tax liability might only require $100,000 to $150,000 in liquid reserves.

Where That Cash Usually Sits

The excess typically ends up in one of three places:

- A high-yield savings account

- A money market fund

- A short-term Treasury or bond fund

These aren't bad tools, but they're the wrong tool for capital that doesn't actually need to be liquid. You're earning interest when you could be building wealth.

The Math: What Excess Cash Actually Costs You

Let's put some numbers to it. Assume you're a Big Law partner who:

- Owes approximately $100,000–$150,000 in quarterly tax payments

- Keeps close to $1,000,000 in cash or cash equivalents throughout the year

- Invests the remainder, if anything, only after year-end

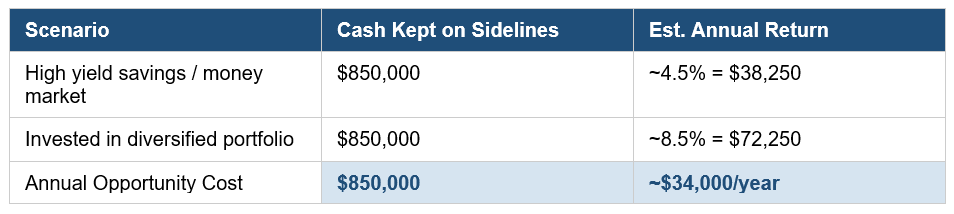

A reasonable liquidity buffer for quarterly taxes and living expenses might be $150,000. That means roughly $850,000 is sitting in cash that could be working for you.

Here's what that opportunity cost looks like on an annual basis:

That's roughly $34,000 per year in foregone growth, just in year one. But the real damage compounds over time:

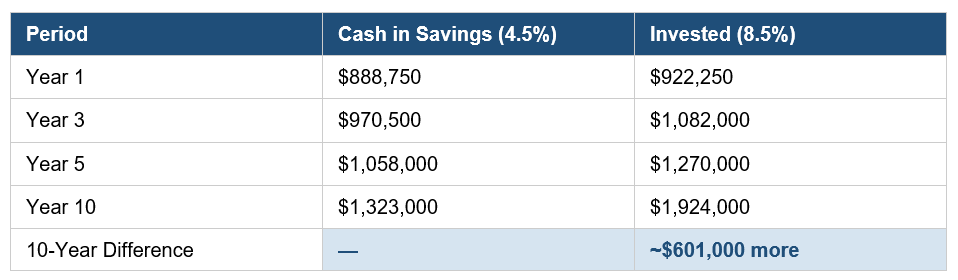

Over a 10-year period, keeping $850,000 in savings instead of invested could cost you over $600,000 in portfolio growth. Enough to nearly pay for an entire year of Door Dashed lunches in NYC.

Why This Keeps Happening

The root cause isn't carelessness; it's the absence of a coordinated plan. Most Big Law partners have two advisors in their corner: a CPA and an investment advisor. The CPA tells you what you owe. The investment advisor manages what you've handed them. But nobody is quarterbacking your cash flow in real time.

Nobody is answering questions like:

- How much liquidity do I actually need right now?

- When should I be moving excess cash into the market?

- Am I over-reserving for taxes because my estimates are off?

- Could some of this capital be working in a brokerage, a real estate investment, or a policy?

Without someone coordinating those answers, the default is always to hold more cash. It's the path of least resistance, and the most expensive one.

What a Better Approach Looks Like

The partners who avoid this trap typically have one thing in common: a financial advisor who functions more like a personal CFO than an investment picker. That means someone who:

- Works alongside your CPA to build a realistic quarterly tax reserve, not a worst-case buffer

- Builds a systematic schedule for deploying excess cash into the market throughout the year

- Evaluates the full picture, brokerage, qualified accounts, real estate, and alternative structures, to make sure your capital is allocated to its highest and best use

- Revisits the plan as your income and tax situation evolve

Investment selection is table stakes. Cash flow coordination is where real wealth is built or lost.

The Final Verdict

If you're a Big Law partner sitting on a large cash position because you're not sure exactly what you'll owe or when, you're not alone, and you're not being irrational. But you may be significantly underestimating the cost of that uncertainty.

The goal isn't to be reckless with liquidity. It's to be precise about how much you actually need, and to put the rest to work.

8933867DH_MAY28