Asset Location vs Asset Allocation

Written by Chris DeVito

Why Your 401(k), IRA, and Brokerage Account Shouldn’t All Look the Same

Most professionals spend time figuring out what to invest in… but almost no time thinking about where they invest it.

If your 401(k), IRA, and brokerage account all hold the same blend of stocks and bonds, you're making a common—and costly—mistake.

💡 The same asset in the wrong account can quietly destroy your after-tax returns.

Strategic investors use asset location—not just allocation—to grow wealth faster and more efficiently.

Not All Accounts Are Taxed the Same

| Account Type | Tax Treatment | Best Used For |

| 401(k) / Traditional IRA | Tax-deferred; pay taxes at withdrawal | High-growth stocks, REITs, taxable bonds |

| Roth IRA / Roth 401(k) | Tax-free growth forever | Highest-growth assets (i.e. tech, small caps) |

| Brokerage Account | Taxed annually on dividends & capital gains | Tax-efficient ETFs, muni bonds, liquidity |

Why Go Heavy on Equities in Your 401(k)

Equities are your highest long-term growth assets. But they also generate the most capital gains—which means taxes… unless they’re in a tax-deferred or tax-free account.

Your 401(k) is the perfect place to concentrate equities because:

- You defer taxes for decades

- There's no annual tax drag from dividends or trades

- You can rebalance aggressively without tax impact

- You maximize compounding inside a protected wrapper

✅ Think of your 401(k) as your growth engine—not your safety net.

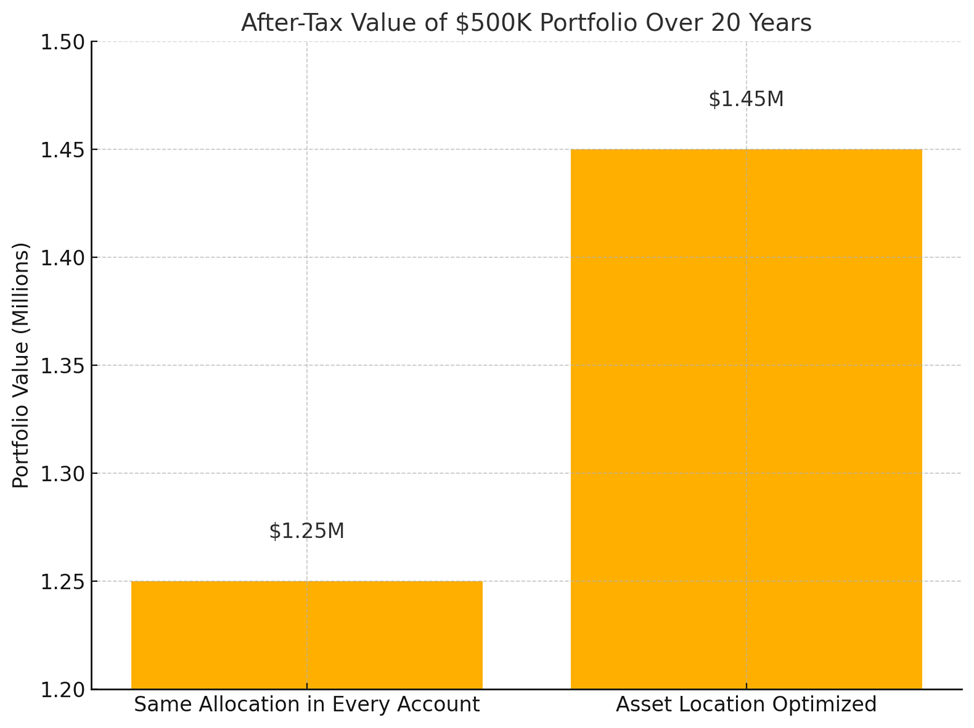

📈 ExamplE: After-Tax Value of Two Portfolios Over 20 Years

- $500,000 total portfolio across 401(k), Roth IRA, and brokerage

- Target allocation: 80% stocks / 20% bonds

- Same investments, different account placement

Portfolio Strategy | Ending After-Tax Value (20 Years) |

Portfolio A: Same allocation in every account (80/20 in each) | $1.25M |

Portfolio B: Asset location optimized (equities in 401(k) and Roth, bonds in IRA, ETFs in brokerage) | $1.45M |

$200,000+ difference just from smarter asset placement.

No additional risk. No extra capital. Just better strategy.

Your New Framework: What Goes Where

Here’s a simplified version of the Asset Location Playbook:

Asset | Ideal Account Type |

U.S. Stocks (Growth) | 401(k), Roth IRA |

Small Cap / Tech Stocks | Roth IRA |

Bonds / REITs | Traditional IRA or 401(k) |

Tax-Efficient ETFs | Taxable brokerage |

Muni Bonds | Taxable brokerage |

Bottom Line: You Don’t Need More Investments. You Need Better Placement.

When high earners clone the same portfolio across accounts, they lose to taxes. But with smart asset location, you can:

✅ Reduce tax drag

✅ Maximize compounding

✅ Increase your long-term wealth—without adding risk

DISCLOSURE: A distribution from a Roth IRA is tax-free and penalty-free, provided the five-year aging requirement has been satisfied and one of the following conditions is met: age 59½, disability, qualified first-time home purchase, or death.

For Educational Purposes Only – Not to be relied upon as financial, tax, or legal advice.

All examples are hypothetical example and not representative of any specific strategy or situation. 8240137RG_Aug27